𝗪𝗵𝘆 𝗜’𝗺 𝗧𝘂𝗿𝗻𝗶𝗻𝗴 𝘁𝗼 𝗚𝗼𝗹𝗱: 𝗣𝗮𝘁𝗶𝗲𝗻𝗰𝗲 𝗮𝗻𝗱 𝗖𝗼𝗻𝘃𝗶𝗰𝘁𝗶𝗼𝗻 𝗶𝗻 𝗮𝗻 𝗢𝘃𝗲𝗿𝘃𝗮𝗹𝘂𝗲𝗱 𝗠𝗮𝗿𝗸𝗲𝘁

𝗪𝗵𝘆 𝗜’𝗺 𝗧𝘂𝗿𝗻𝗶𝗻𝗴 𝘁𝗼 𝗚𝗼𝗹𝗱: 𝗣𝗮𝘁𝗶𝗲𝗻𝗰𝗲 𝗮𝗻𝗱 𝗖𝗼𝗻𝘃𝗶𝗰𝘁𝗶𝗼𝗻 𝗶𝗻 𝗮𝗻 𝗢𝘃𝗲𝗿𝘃𝗮𝗹𝘂𝗲𝗱 𝗠𝗮𝗿𝗸𝗲𝘁

𝗢𝗰𝘁𝗼𝗯𝗲𝗿 𝟭𝟬, 𝟮𝟬𝟮𝟱

For several months now, global stock markets have reached historically high valuation levels.

Large-cap tech companies continue to push the indices upward, but behind the shine lies a clear reality: risk has become disproportionate to potential return.

Even Warren Buffett, through Berkshire Hathaway, is holding $ 357 billion in cash, representing 27% of his investment capacity — clear evidence that he, too, considers the market too expensive to invest in heavily.

In this environment of extreme valuations, I prefer prudence and tangibility.

That’s why I’ve chosen to focus my exposure on gold mining equities, for three main reasons.

𝗔𝗻 𝗘𝘅𝗽𝗹𝗼𝘀𝗶𝘃𝗲 𝗠𝗮𝗰𝗿𝗼𝗲𝗰𝗼𝗻𝗼𝗺𝗶𝗰 𝗮𝗻𝗱 𝗣𝗼𝗹𝗶𝘁𝗶𝗰𝗮𝗹 𝗘𝗻𝘃𝗶𝗿𝗼𝗻𝗺𝗲𝗻𝘁

We are entering a phase of global instability:

- Renewed trade wars initiated by the United States;

- Persistent geopolitical tensions (Ukraine, the Middle East, Asia);

- Domestic political crises in Europe (notably in France), weakening the eurozone;

- Risk of stagflation in the U.S., as highlighted by Larry Fink (BlackRock).

Each time uncertainty dominates, capital flows back into gold — a universal store of value, independent of any political system.

𝗖𝗲𝗻𝘁𝗿𝗮𝗹 𝗕𝗮𝗻𝗸𝘀 𝗔𝗿𝗲 𝗕𝘂𝘆𝗶𝗻𝗴 𝗚𝗼𝗹𝗱 𝗟𝗶𝗸𝗲 𝗡𝗲𝘃𝗲𝗿 𝗕𝗲𝗳𝗼𝗿𝗲

Over the past three years, non-Western central banks (China, Russia, Turkey, India, and others) have pursued a clear de-dollarization policy:

- They seek to reduce their dependence on the U.S. dollar, now used as a geopolitical weapon;

- They have massively accumulated gold, with over 1,000 tonnes purchased in recent years;

- The World Gold Council reports that 43% of central banks plan to increase their gold reserves within the next 12 months.

- This is a structural, deep, and lasting trend — not a passing fad.

𝗟𝗼𝘄 𝗥𝗲𝗮𝗹 𝗥𝗮𝘁𝗲𝘀 𝗮𝗻𝗱 𝗚𝗹𝗼𝗯𝗮𝗹 𝗗𝗲𝗯𝘁 𝗦𝘂𝗽𝗽𝗼𝗿𝘁 𝘁𝗵𝗲 𝗬𝗲𝗹𝗹𝗼𝘄 𝗠𝗲𝘁𝗮𝗹

Major economies, particularly the United States, are trapped by debt:

- U.S. debt equals ~120% of GDP, with $ 1 trillion in annual interest payments;

- Raising rates significantly would trigger a fiscal crisis;

As a result, real interest rates are likely to remain low for an extended period.

Gold may not generate yield, but it loses less value when rates decline.

It remains a store of purchasing power — an asset uncorrelated with equities and immune to counterparty risk.

𝗠𝘆 𝗖𝘂𝗿𝗿𝗲𝗻𝘁 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝘆 :

I remain exclusively exposed to gold mining equities in the short to medium term.

I’m waiting for a true buying opportunity - a deep correction - before reallocating to traditional equity markets.

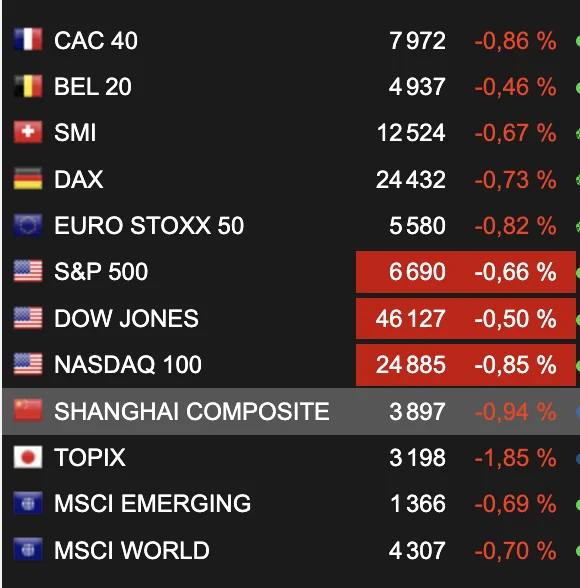

As shown below, all major stock indices are currently affected.

$NSDQ100 $SPX500 $GOLD

⚠️ Risk Disclaimer:

This is a personal investment strategy, not financial advice.

Whether you choose to apply it or not is entirely up to you.

Past performance does not guarantee future results.